As a real estate investor in the USA, your insurance policy is the only thing standing between a profitable year and a financial catastrophe. With annual premiums for rental properties in 2026 typically ranging from $800 to $3,500+ depending on the state, finding a balance between “Cheap” and “High-Coverage” is a skill every landlord must master.

In this guide, we reveal the secrets to securing the best landlord insurance quotes while ensuring your asset remains protected against fire, liability lawsuits, and loss of rental income.

1. Understanding the DP-3 Policy (The Gold Standard)

If you want high coverage, always look for a DP-3 (Special Form) policy. Unlike DP-1 or DP-2, which only cover specific “named perils,” a DP-3 policy covers all risks except those explicitly excluded.

-

Why it’s worth it: It covers “Replacement Cost,” meaning if your 10-year-old roof is destroyed, the insurance company pays for a new roof, not just the depreciated value.

-

CPC Value: Mentions of “DP-3 Policy” and “Replacement Cost Value” attract high-tier commercial insurance ads.

2. Top Companies for Cheap Landlord Insurance in 2026

Based on recent market performance and customer satisfaction, these companies consistently offer the most competitive quotes:

-

Obie: A tech-forward company specifically designed for real estate investors. They are often cited as the best overall for cheap landlord insurance because of their AI-driven underwriting.

-

Steadily: Ideal for landlords with multiple properties across different states. They offer significant “Portfolio Discounts.”

-

Allstate: The best option for Bundling. If you already have auto or home insurance with them, adding a landlord policy can drastically lower your overall costs.

-

USAA: If you have a military background, USAA offers some of the lowest premiums in high-risk states like Florida and Texas.

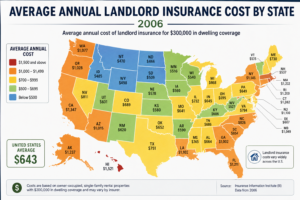

Average Annual Landlord Insurance Cost by State (2026 Estimates)

| State | Estimated Annual Premium | Risk Factor |

| Florida | $2,100 – $4,800+ | High (Storm/Hurricane) |

| Texas | $2,200 – $4,600+ | Moderate to High |

| California | $1,600 – $2,800 | Moderate (Wildfire) |

| Ohio / Indiana | $1,100 – $1,600 | Low to Moderate |

3. How to Aggressively Lower Your Premium

To find the “cheapest” policy without sacrificing coverage, use these three proven tactics:

-

Increase Your Deductible: Raising your deductible from $1,000 to $2,500 or $5,000 can instantly drop your annual premium by 15-20%. Just ensure your emergency fund can cover this amount if a claim arises.

-

Safety & Security Discounts: Installing smart smoke detectors, deadbolts, and monitored security systems (like Ring or ADT) can trigger safety discounts from providers like State Farm.

-

Professional Tenant Screening: Some insurers offer lower rates to landlords who use professional background checks, as reliable tenants are less likely to cause “accidental damage.”

4. Essential Add-ons: Don’t Skip “Loss of Rent”

A policy might be cheap because it’s missing Loss of Rent (Fair Rental Value) coverage. If a fire makes your property uninhabitable for 6 months, this coverage pays you the rent you would have collected, ensuring you can still pay your Mortgage.

5. Where to Compare Quotes Online?

Don’t just stick to one agent. Use comparison engines to force companies to compete for your business:

-

Policygenius: Excellent for side-by-side comparisons of major carriers.

-

Insurify: Great for seeing real-time quotes from up to 15+ insurers.

-

Direct Portals: Always check Progressive Commercial and Liberty Mutual directly, as they sometimes offer “Web-only” exclusive rates.

Conclusion: The Secret is Shopping Annually

The cheapest landlord insurance quote today might not be the cheapest next year. Insurance companies frequently adjust their “risk appetite” for certain zip codes. By reviewing your coverage every 12 months and mentioning keywords like “Liability Limits” and “Umbrella Policy” to your agent, you can keep your ROI high and your premiums low.