In the fast-paced world of US real estate flipping, your choice of financing can be the difference between a $50,000 profit and a foreclosed project. As we navigate the 2026 housing market, the debate between Hard Money Lenders and Traditional Banks has intensified. While banks offer lower interest rates, hard money provides the speed necessary to secure distressed properties before competitors.

This guide breaks down the pros, cons, and 2026 interest rate trends for both financing models to help you choose the best “Capital Structure” for your next flip.

1. Hard Money Lenders: The Speed of Private Capital

Hard money loans are asset-based loans secured by the property itself. They are provided by private companies rather than institutional banks like Wells Fargo or Citibank.

-

Speed is King: In 2026, top lenders like Kiavi or Easy Street Capital can fund a deal in as little as 48 to 72 hours.

-

Focus on ARV: Hard money lenders care more about the After-Repair Value (ARV) than your personal credit score. They often fund up to 90% of the purchase price and 100% of the renovation costs.

-

2026 Rate Trend: Currently, hard money rates range from 8.5% to 12%, which is higher than banks, but the “No-Appraisal” options make them unbeatable for auctions.

2. Traditional Banks: The Low-Cost but Slow Route

If you have a high credit score (720+) and are not in a rush, traditional financing through a conventional mortgage or a Business Line of Credit might be cheaper.

-

Lower Interest Rates: Conventional investment loans in 2026 are hovering around 6.2% to 7.5%.

-

The Catch: Banks require extensive documentation, including 2 years of tax returns and a full property appraisal. Closing can take 30 to 45 days—by which time a “hot” flip is usually gone.

-

Best for: “Fix and Hold” strategies where you intend to keep the property as a rental after renovation (BRRRR Method).

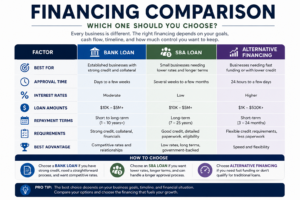

Financing Comparison: Which One Should You Choose?

| Feature | Hard Money Lenders | Traditional Banks |

| Approval Time | 2 – 7 Days | 30 – 60 Days |

| Credit Requirement | Flexible (600+) | Strict (700+) |

| Interest Rates | 8% – 13% | 6% – 8% |

| LTC (Loan to Cost) | Up to 90% | Typically 75% – 80% |

| Origination Fees | 1.5% – 3.5% | 0.5% – 1.5% |

3. Top Hard Money Lenders for Flippers in 2026

If you decide that speed is your priority, these are the most reliable names in the US market:

-

Kiavi (formerly LendingHome): Best for professional flippers looking for “Volume Discounts.”

-

RCN Capital: Known for the lowest starting rates in the hard money sector.

-

Lima One Capital: Offers excellent “Fix-and-Flip” to “Rental” transition loans.

4. Hybrid Strategy: The Bridge Loan

Many investors in 2026 are using Bridge Loans. This is a short-term financing option that “bridges” the gap until you can secure long-term financing or sell the property. It combines the speed of hard money with a slightly more structured approach, often used for “Mid-sized” multi-family flips.

5. Hidden Costs to Watch Out For

When comparing quotes, don’t just look at the interest rate. Check for:

-

Draw Fees: How much the lender charges every time they release money for renovations.

-

Prepayment Penalties: Some traditional banks charge you if you sell the house too fast (within 6 months).

-

Points: One “point” equals 1% of the loan amount. Hard money lenders usually charge 1-3 points upfront.

Conclusion: The Winner Depends on the Deal

If you find a deeply discounted property at a foreclosure auction, Hard Money is your only real choice. However, if you are buying a property that doesn’t need much work and the seller is willing to wait, a Traditional Bank will save you thousands in interest.